The "Lock-In Effect" vs. Lifestyle: Why Americans Are Still Moving

The Mortgage Lock-In Effect has transformed domestic migration from a casual lifestyle choice into a precise mathematical calculation, forcing modern households to trade regional tax rates against lifetime interest penalties.

The "Lock-In Effect" vs. Lifestyle: Why Americans Are Still Moving

The residential real estate market faces a structural paradox. A vast segment of homeowners are financially bound to their current properties by what economists call the "Lock-In Effect." Having secured historic, ultra-low fixed mortgage rates below 4% prior to macroeconomic shifts, these individuals face a steep financial hurdle if they choose to sell and re-enter the market at contemporary, elevated rates.

On paper, this economic friction should paralyze domestic migration. Yet, municipal data tells a completely different story.

Americans are still moving in record numbers, but the nature of migration has fundamentally shifted. Moving is no longer casually speculative; it has become intensely lifestyle-driven and intentional. When the structural affordability gap between two geographic regions becomes wide enough, it overrides the financial penalty of abandoning a legacy mortgage. Here is an analysis of the demographic forces driving domestic migration and where the population is shifting.

1. Quantifying the Mortgage Lock-In Penalty

To understand why a consumer chooses to move despite adverse market conditions, we must look at the mathematical reality of the lock-in penalty.

When a household relinquishes a 3.2% fixed interest rate on a $350,000 balance to purchase an equivalently priced home at contemporary market rates hovering near 6.5% to 7%, their monthly principal and interest payment jumps by roughly $700 to $800. This is an immediate, structural erosion of household purchasing power.

For migration to occur against this financial headwind, the destination municipality must offer an offsetting economic advantage. Typically, this advantage manifests in two distinct forms:

- Severe Cost-of-Living Deltas: Moving from a hyper-expensive tier-1 metropolitan area to a high-growth regional hub where everyday consumer costs are 20% to 35% lower.

- Asset Liquidation Arbitrage: Selling a highly appreciated property in an inflated coastal market and using the accumulated equity to purchase a home in cash within a lower-cost state, completely bypassing the contemporary mortgage ecosystem.

2. Short-Distance Downscaling vs. Long-Distance Arbitrage

The intentional migration wave splits cleanly into two distinct geographic behaviors, as tracked by municipal population registries. While localized, short-distance moves (within the same county or adjacent suburbs) have slowed significantly due to transactional friction, long-distance interstate relocations remain highly active. Consumers are concluding that if they must break their legacy mortgage rate, they might as well make the move count by completely shifting to an optimized economic environment.

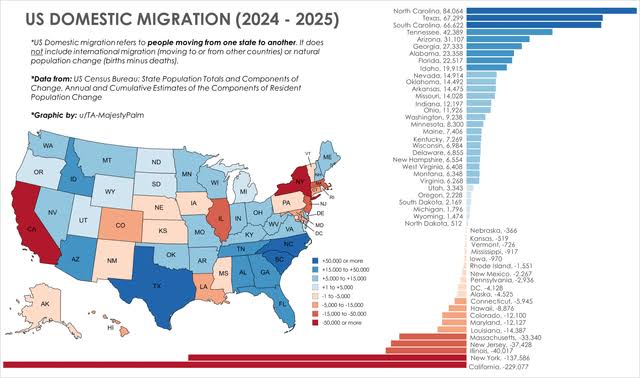

U.S. Domestic Migration Shifts by State. Source: Reddit

As visualized in the tracking map above, the domestic migration trend displays a distinct blue-to-orange gradient shift. High-cost hubs like California and New York are experiencing consistent population contraction as households opt out of localized infrastructure strains. Meanwhile, destination corridors across the Southeast and Mountain West are maintaining a steady influx of residents looking to maximize geographic purchasing power.

3. The Top Inbound Lifestyle Destinations

The ongoing population reallocation favors specific regional corridors that successfully balance robust employment infrastructure with lifestyle amenities and favorable state tax frameworks.

1.Evaluate State-Level Tax Architecture: Filter 1.

Inbound populations prioritize states with structural fiscal advantages, such as no state income tax (e.g., Florida, Texas, Nevada) or highly conservative corporate tax rates (e.g., North Carolina).

2.Analyze Housing Inventory Trajectories: Filter 2.

Smart movers target regions experiencing aggressive residential construction. Increased inventory stabilizes price-per-square-foot metrics, preventing the hyper-competitive bidding wars seen in land-locked coastal cities.

3.Map Climate and Environmental Value: Filter 3.

The "Sunbelt Shift" persists because consumers are actively trading high-density, harsh-winter environments for milder climates that support year-round outdoor lifestyle activities and reduce home heating utility burdens.

4.Verify Municipal Infrastructure Readiness: Filter 4.

Relocating professionals favor mid-sized cities adjacent to major metros—places that boast high-capacity broadband infrastructure, localized airport access, and modern medical networks without urban crowding.

4. Cross-Regional Migration Metrics

When analyzing the economic profiles of primary inbound regions, clear data patterns emerge regarding population influx and real estate baseline metrics:

|

Targeted Inbound Region |

Dominant Growth Driver |

Average Cost of Living Index |

Net Population Inflow Trend |

|

Southeast Corridor (e.g., North Carolina, Florida) |

Corporate relocation & zero/low state income tax |

92% – 98% (Below national baseline) |

High Acceleration |

|

Mountain West (e.g., Arizona, Idaho, Nevada) |

Space optimization & outdoor lifestyle access |

102% – 106% (Moderate) |

Steady Growth |

|

Midwest Tech Hubs (e.g., Ohio, Indiana regional centers) |

Extreme affordability & manufacturing revitalization |

84% – 89% (Highly affordable) |

Emerging Influx |

5. The Long-Term Outlook for Municipal Planning

For businesses, real estate investors, and data platforms like Urblytica, tracking these intentional moves is vital. The traditional reliance on historic migration baselines is no longer reliable. When citizens move today, they are executing precise, calculated adjustments to their household balance sheets.

Municipalities that fail to invest in infrastructure, or those that maintain highly restrictive zoning laws that suppress new housing starts, will see their tax bases gradually erode. Meanwhile, forward-thinking mid-tier cities that welcome development and maintain low administrative friction will continue to capture the highly liquid, educated, and intentional workforce driving the modern economy.

Put Your Brand in Front of Movers & Founders

Reach a high-intent relocation and business audience across thousands of cities. Claim your space today.

View Placement Rates →